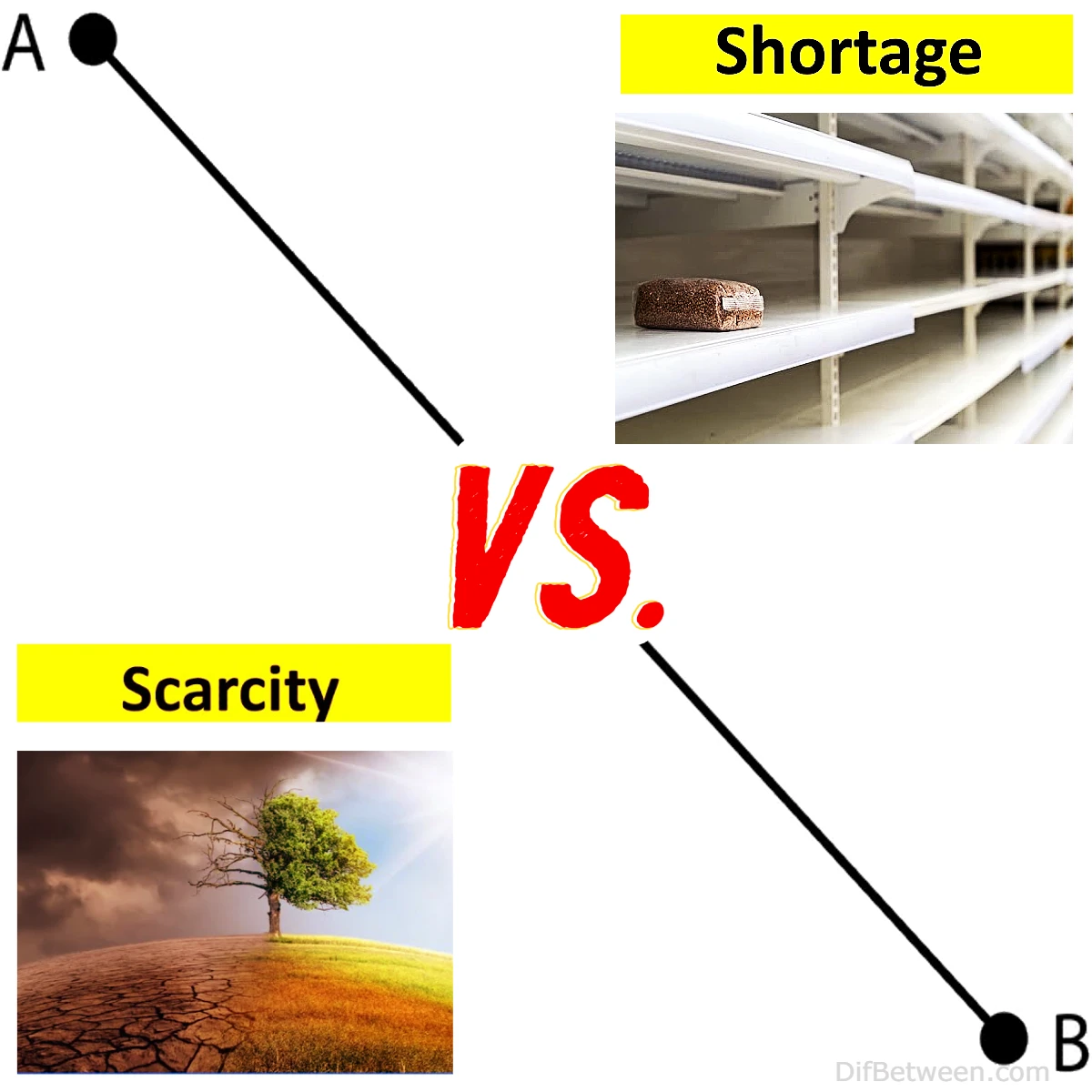

| Aspect | Scarcity | Shortage |

|---|---|---|

| Meaning | Inherent limitation of resources | Temporary imbalance between demand and supply |

| Duration | Constant economic condition | Short-term phenomenon |

| Nature | Fundamental economic principle | Market-specific occurrence |

| Cause | Limited resources, population growth, technological advancements | Supply disruptions, seasonal demand, government intervention |

| Resolution | Resource allocation, trade-offs | Market equilibrium, supply restoration |

| Implications | Drives decision-making, resource allocation, and innovation | Disrupts markets, causes price fluctuations, and requires policy responses |

| Strategies | Resource efficiency and conservation, diversification and substitution, investment in R&D, international trade and cooperation | Increasing supply, demand management, inventory management, collaboration and coordination |

| Examples | Scarcity of natural resources (water, fossil fuels), scarcity of skilled labor, scarcity of arable land | Shortage of medical supplies, shortage of housing during a crisis, shortage of seasonal goods |

Today, we embark on a captivating journey through the realms of economics as we explore the fascinating differences between scarcity and shortage. In a world where resources are limited, understanding these concepts is vital for navigating the complexities of supply and demand. So, let’s dive in and uncover the nuances of scarcity and shortage!

Imagine a world where desires are boundless, but resources are finite. This is the essence of scarcity, the fundamental economic principle that shapes our choices and trade-offs. Scarcity highlights the inherent limitation of resources relative to the unlimited wants and needs of individuals, businesses, and societies. It forces us to prioritize, make difficult decisions, and seek ways to optimize the use of scarce resources. But what about shortage? Unlike scarcity, which is a constant economic condition, shortage refers to a temporary imbalance between the demand and supply of a specific good or service in a particular market. Shortages can arise from various factors like supply disruptions, seasonal demand fluctuations, or even government intervention. They disrupt the normal functioning of markets and often lead to price fluctuations, rationing, and market uncertainties. However, it’s crucial to remember that shortages are not everlasting and can be resolved over time.

Understanding the distinctions between scarcity and shortage empowers us to make informed decisions and navigate the ever-changing economic landscape. By recognizing the impact of scarcity, we can embrace resource efficiency, innovation, and responsible consumption. When shortages arise, proactive measures such as increasing supply, demand management, and effective collaboration can help mitigate their effects. So, dear readers, join me on this enlightening exploration as we deepen our understanding of scarcity versus shortage. Together, let’s unravel the complexities of economics and forge a path towards sustainable resource management. Read on to delve into the intricacies of scarcity and shortage!

Scarcity: The Fundamental Economic Principle

Definition and Concept of Scarcity

Scarcity lies at the very heart of economics. It refers to the inherent limitation of resources in the face of unlimited wants and needs. In other words, scarcity implies that there is a finite supply of resources (such as land, labor, capital, and natural resources) relative to the infinite demand for goods and services.

Understanding Scarcity

To grasp the concept of scarcity, imagine a scenario where you have a single pie and a group of hungry friends. As much as everyone desires a slice, there’s only so much pie to go around. This scenario exemplifies scarcity in action. The scarcity of the pie necessitates making choices and trade-offs, as not everyone can have as much pie as they desire.

Scarcity compels individuals, businesses, and governments to make decisions about resource allocation. It forces us to prioritize and make trade-offs to satisfy our most pressing needs and wants. Understanding scarcity is crucial for comprehending how economies function and how individuals make rational choices.

Factors Contributing to Scarcity

Several factors contribute to the existence of scarcity. Let’s explore a few of the key drivers:

- Limited Resources: Scarce resources include natural resources (like oil, minerals, and forests), human resources (labor and skills), capital goods (machinery and equipment), and land. These resources have finite quantities and can be depleted or exhausted over time.

- Increasing Population: As the global population continues to grow, the demand for resources intensifies. More people vying for the same resources exacerbates scarcity.

- Technological Advancements: While technology enhances productivity and efficiency, it does not eliminate scarcity. Instead, it often creates new demands and desires, further fueling the scarcity of resources.

Now that we have a solid understanding of scarcity, let’s turn our attention to shortage.

Shortage: A Temporary Imbalance

Definition and Concept of Shortage

Shortage refers to a temporary imbalance between the demand and supply of a particular good or service in a specific market. Unlike scarcity, which is a fundamental economic condition, shortages are short-term phenomena that can be resolved over time.

Characteristics of Shortage

Shortages are characterized by a few key elements:

- Insufficient Supply: A shortage occurs when the quantity of a product or service demanded by consumers exceeds the quantity available for sale by suppliers.

- Market Disruption: Shortages often disrupt the normal functioning of the market. They can lead to price increases, rationing, long waiting times, and a surge in demand from consumers seeking to secure the limited supply.

- Temporary Nature: Shortages are not perpetual. They occur due to specific circumstances such as production disruptions, supply chain issues, natural disasters, or sudden changes in consumer preferences. Once these factors are resolved, the market tends to return to equilibrium.

Causes of Shortage

Shortages can arise from various factors. Let’s take a closer look at some common causes:

- Supply Disruptions: Unexpected events, such as natural disasters, accidents, or strikes, can disrupt the production or distribution of goods and services, leading to shortages.

- Seasonal or Cyclical Demand: Certain products may experience seasonal or cyclical fluctuations in demand. For example, the demand for heating fuel rises during the winter, potentially resulting in shortages if the supply is not adequately prepared.

- Government Intervention: Government policies, regulations, or price controls can distort the supply-demand balance, causing shortages. For instance, price ceilings set below the market equilibrium can lead to increased demand and reduced supply.

Differences Between Scarcity and Shortage

Now that we’ve explored the nuances of scarcity and shortage, let’s summarize the key differences between the two in a handy table:

| Aspect | Scarcity | Shortage |

|---|---|---|

| Meaning | Inherent limitation of resources | Temporary imbalance between demand and supply |

| Duration | Constant economic condition | Short-term phenomenon |

| Nature | Fundamental economic principle | Market-specific occurrence |

| Cause | Limited resources, population growth, technological advancements | Supply disruptions, seasonal demand, government intervention |

| Resolution | Resource allocation, trade-offs | Market equilibrium, supply restoration |

Implications of Scarcity

Opportunity Cost and Trade-offs

Scarcity gives rise to the concept of opportunity cost, which refers to the value of the next best alternative forgone when making a choice. When resources are scarce, individuals, businesses, and governments must make trade-offs, sacrificing one option in favor of another. For example, a government may choose to allocate resources to healthcare instead of infrastructure development, recognizing that the scarcity of resources requires prioritization.

Price Mechanism and Resource Allocation

Scarcity plays a crucial role in the price mechanism, which determines how resources are allocated in a market economy. When a resource becomes scarce, its price tends to rise due to increased demand and limited supply. Higher prices signal to consumers that the resource is scarce, encouraging them to use it more efficiently and incentivizing producers to increase its production. In this way, scarcity influences resource allocation through market forces.

Innovation and Resource Management

Scarcity drives innovation and resource management efforts. When resources become scarce, individuals and organizations are motivated to find alternative ways to fulfill their needs and wants. This leads to the development of new technologies, practices, and techniques that optimize resource utilization. For instance, the scarcity of fossil fuels has spurred research and investment in renewable energy sources as a more sustainable alternative.

Consequences of Shortage

Price Fluctuations and Rationing

Shortages often result in price fluctuations as demand outstrips supply. Suppliers may increase prices to manage the limited quantity available and to allocate the product to those who value it the most. This can lead to higher costs for consumers and potential affordability issues. In some cases, governments may intervene to prevent excessive price increases or implement price controls, which can create further distortions in the market.

Rationing is another common consequence of shortages. It involves distributing the limited supply of a product or service among consumers based on predetermined criteria. Rationing mechanisms can include quotas, coupons, or priority systems. While rationing ensures a more equitable distribution, it may not fully address the underlying issue of insufficient supply.

Market Disruptions and Uncertainty

Shortages disrupt the normal functioning of markets, causing uncertainty and instability. Suppliers may struggle to meet the sudden surge in demand, leading to delayed or limited availability of products. Consumers, faced with scarcity, may resort to panic buying or hoarding, exacerbating the shortage. These disruptions can have ripple effects across related industries and supply chains, affecting prices, employment, and overall economic stability.

Policy Implications

Shortages often prompt policymakers to intervene and implement measures to alleviate the imbalances. Governments may take actions such as increasing production, relaxing regulations, or facilitating imports to address the shortage. However, these interventions must be carefully managed to avoid unintended consequences or long-term distortions in the market. Balancing short-term relief with long-term sustainability is a key challenge for policymakers when dealing with shortages.

FAQs

Scarcity is a fundamental economic condition that arises from the inherent limitation of resources relative to unlimited wants and needs. It is a constant state and requires trade-offs and resource allocation. Shortage, on the other hand, refers to a temporary imbalance between demand and supply of a specific good or service in a particular market. It disrupts market dynamics and can lead to price fluctuations and uncertainties.

Scarcity forces individuals, businesses, and governments to make choices and trade-offs. Since resources are limited, decision-makers must prioritize their needs and wants. They must consider opportunity costs, which involve giving up the next best alternative when making a choice. Scarcity influences decision-making by highlighting the need to optimize resource utilization and make rational choices based on limited availability.

To address scarcity, strategies such as resource efficiency and conservation are crucial. This involves using resources in a sustainable manner, minimizing waste, and optimizing their use. Diversification and substitution of resources can also mitigate the effects of scarcity by reducing reliance on a single resource. Investment in research and development (R&D) promotes innovation and the discovery of alternative resources or technologies. Additionally, international trade and cooperation can help access resources that may be scarce domestically.

Shortages can be resolved by increasing the supply of the goods or services in demand. This can involve incentivizing producers, removing barriers to entry, and facilitating the expansion of production capacity. Demand management techniques, such as price adjustments or implementing measures to discourage hoarding, can help balance demand and supply. Effective inventory management practices and collaboration among stakeholders also play a role in addressing shortages.

Yes, shortages are typically temporary. They occur due to specific circumstances such as supply disruptions, seasonal demand fluctuations, or sudden changes in consumer preferences. Once these factors are resolved, the market tends to return to equilibrium, alleviating the shortage. However, it’s important to note that some shortages may persist if the underlying factors are not effectively addressed.

Read More:

Contents